We are going to review of the Eurozone PMIs as an entity

HCOB Eurozone Composite PMI

Data were collected 10-25 April

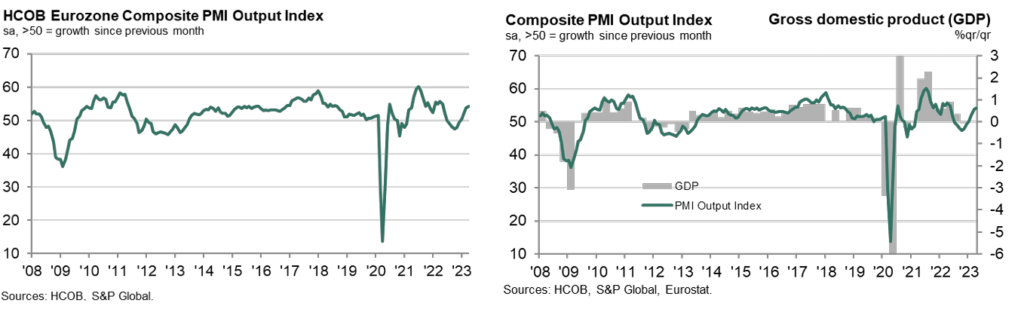

The eurozone economy recorded a further monthly expansion in economic activity at the start of the second quarter, extending the expansionary sequence seen since the start of 2023, the latest HCOB PMI® survey showed. In fact, growth strengthened to an 11-month high, signalling a further gaining of momentum following accelerated upturns in both February and March.

April’s robust increase in output solely reflected growth in services activity, however, as manufacturing production fell for the first time since January. Similarly, a strong improvement in demand for services offset beleaguered manufacturing sector order books, which shrank again.

Nevertheless, euro area employment growth picked up to just shy of a one-year high, while inflationary pressures continued to subside. Input price pressures, albeit still historically sharp, eased to a 26-month low. Output prices were subsequently lifted to the softest extent in two years. The seasonally adjusted HCOB Eurozone Composite PMI Output Index increased to 54.1 in April from 53.7 in March.

The latest survey results confirmed a fourth consecutive month where the headline index has been above the crucial 50.0 level and therefore indicative of growth in business activity. Moreover, April’s expansion was the fastest in nearly a year as the upturn gathered momentum for a third month in a row.

Of the countries with Composite PMI data available (which together account for around 78% of eurozone private sector output), the latest HCOB survey showed broad-based growth in April.

Spain was once again the fastest-growing euro area economy, although the expansion did ease slightly from March’s 16-month high. Italy registered a strong upturn in April, with growth close to a one-and-a-half-year high.

Stronger momentum was also seen in the euro area’s largest economy, Germany, which compared with a softer and modest expansion in France.

Supporting greater euro area business activity levels in April were improving demand conditions. New order inflows picked up for a third consecutive month, rising moderately and at the quickest pace since May 2022. That said, higher new business was limited to domestic sources, according to the latest survey data, as new export orders* fell for a fourteenth month in a row.

The decline in sales to foreign customers did ease, however, to the weakest in close to a year. Notably, the rise in business activity continued to outpace that seen for new orders. Consequently, April survey data highlighted a reduction in companies’ backlogs of work, the ninth in the past ten months. Firms were able to tackle their unfilled orders thanks to a further expansion in capacity as employment across the eurozone increased for a twenty-seventh successive survey period. The rate of job creation picked up to the strongest since May last year.

Euro area businesses remained optimistic towards the next 12 months, with growth expectations roughly in line with their long-run average. However, the degree of positivity weakened slightly to a three-month low.

Countries ranked by Composite PMI Output Index: April

Spain 56.3 2-month low

Italy 55.3 17-month high

Germany 54.2 (flash 53.9) 12-month high

Ireland 53.5 2-month high

France 52.4 (flash: 53.8) 2-month low *includes intra-eurozone trade

For complete information check pmi.spglobal.com

Check our post about A.P. Moller – Maersk 2023 Q1 results

{kind=link}

{kind=link}