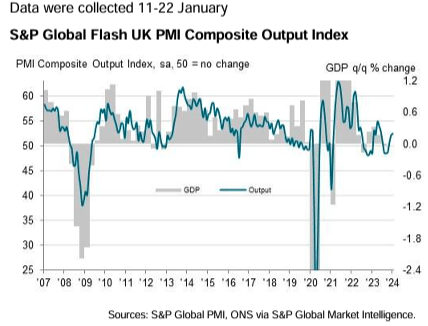

S&P Global just release the UK PMI survey In January, there was a more robust increase in the output of the UK private sector compared to the end of 2023. This was primarily driven by a continued recovery in the service economy.

UK PMI

The surge in service sector activity marked the fastest pace since May of the previous year, while manufacturing production experienced its most significant decline in three months. The most recent survey also pointed to a modest resurgence in private sector employment at the beginning of 2024. This was fueled by improving demand conditions and heightened optimism regarding the business outlook.

In the interim, private sector enterprises documented the most notable surge in input expenses since August 2023, spurred by renewed cost challenges within the manufacturing domain. Reports abound regarding escalated freight costs following the Red Sea crisis.

Additionally, worldwide shipping delays resulted in an extension of suppliers’ delivery timelines, marking the initial occurrence in 12 months and the most significant elongation since September 2022.

Service sector activity

A robust uptick in service sector activity played a pivotal role in enhancing private sector output at the beginning of the year. The pace of expansion quickened to its most rapid in eight months.

Respondents in the survey largely remarked on heightened confidence among clients, with some noting a reversal in demand dynamics due to reduced borrowing costs. In contrast to the favorable trajectory in the service economy, manufacturing production continued its decline for the eleventh consecutive month, reaching its swiftest descent since October. This was frequently attributed to insufficient order volumes and customers holding excess inventory.

Private sector employment

Data from January indicated a slight increase in private sector employment, marking the conclusion of a four-month stretch of job reductions. The elevated staffing levels were indicative of a resurgence in recruitment within the service sector, a trend linked by survey respondents to the commencement of new projects and anticipated growth in demand.

However, numerous reports still highlighted instances of workforce redundancies and the non-replacement of voluntary departures, particularly within the manufacturing sector. This was frequently attributed to robust wage pressures and an excess of business capacity, underscored by a continued reduction in work backlogs across the private sector in January.

Red Sea crisis

The manufacturing supply chains experienced disruptions due to prolonged waiting times for container freight in January following the Red Sea crisis. The most recent data indicated the most significant extension in vendor delivery times since September, putting an end to an eleven-month streak of consistent improvement. Supplier delays were primarily associated with longer international shipping times, driven by vessels rerouting away from the Suez Canal. Concurrently, preproduction inventories saw the most substantial decrease since last August as safety stocks were depleted.

Escalating ocean freight rates played a role in a significant uptick in cost burdens within the manufacturing sector in January, marking the highest inflation rate since March 2023. While factory gate prices saw only a modest increase, it was notable as it occurred at the joint-fastest pace in eight months.

More information S&P Global