Santander reports attributable profit of €5,241 million for the first half of 2023, increasing earnings per share by 13%

Santander report key performance

• During the last twelve months, the bank has successfully added nine million customers, leading to a 4% increase in deposits.

• The bank’s revenues have experienced a substantial 13% growth, supported by strong income expansion across all regions and global businesses. Notably, Santander CIB saw a remarkable growth of 24%, while Wealth Management & Insurance and PagoNxt achieved growth rates of 25% and 27%, respectively.

• Net interest income has risen by 15%, reflecting increased customer activity and the positive impact of higher interest rates in Europe on the balance sheet.

• Fee income has seen a healthy increase of 5%, primarily driven by growth in payments, Santander CIB, and Wealth Management & Insurance, which highlights the strength of the group’s global businesses.

• Despite inflationary pressures, the bank has managed to improve its efficiency ratio further to 44.2%. This improvement is attributed to the bank’s transformation towards a simpler and more integrated model, leading to enhanced profitability.

• Loan-loss provisions have increased by 21%, mainly due to the normalization after the pandemic in the US. However, compared to the previous quarter, provisions in the second quarter decreased in the US, demonstrating better-than-expected credit quality.

• The overall credit quality remained robust, with the cost of risk lower than the annual target at 1.08%.

• In the second quarter, the bank achieved an attributable profit of €2,670 million, which represents a significant 17% increase. In comparison to the first quarter, profit rose by 4%.

• The bank successfully completed its second share buyback against 2022 earnings in April. Since November 2021, the group has bought back 7% of its shares. The combined value of buybacks and cash dividends over the past year equates to a yield of over 8%.

• Santander is well on track to achieve its 2023 targets, which include double-digit income growth, a RoTE above 15%, a cost-to-income ratio of 44-45%, fully-loaded CET1 above 12%, and a cost of risk below 1.2%.

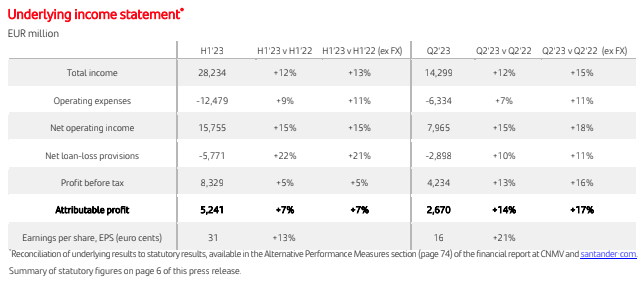

Santander underlying income statement*

During the first half of 2023, Santander achieved notable financial performance, with an attributable profit of €5,241 million, showing a 7% increase in both constant and current euros compared to the same period in the previous year. This growth was primarily driven by strong revenue expansion, particularly in Europe, which helped to offset the year-on-year growth in provisions in North and South America.

In the second quarter of 2023, the bank’s attributable profit rose by 17% compared to the second quarter of 2022, reaching €2,670 million. This growth can be attributed to a significant increase in the number of customers served by the group, with a remarkable addition of nine million customers year-on-year, resulting in a total customer base of 164 million.

The bank’s strong financial results translated into growing profitability and shareholder value. The return on tangible equity (RoTE) reached an impressive 14.5%, showing an increase of 80 basis points. Earnings per share (EPS) also experienced positive growth, reaching 31 euro cents, a rise of 13% compared to the previous year. Additionally, the tangible net asset value (TNAV) per share stood at €4.57 as of June 30th.

When considering the cash dividends paid against 2022, the TNAV per share plus cash dividend per share increased by 11% year-on-year. Notably, in the first six months of the year, the value created for shareholders, which includes TNAV and cash dividends, amounted to more than €6 billion, demonstrating the bank’s commitment to creating value for its investors.

Overall, Santander’s strong financial performance during this period underscores its ability to deliver sustainable growth and generate significant shareholder value.

Market summary (H1 2023 vs H1 2022)

The group’s strategic diversification across geographic regions and business segments remains a driving force behind its consistent and profitable growth. The strong performance in Europe during the first half of the year effectively balanced out the year-on-year increase in provisions observed in North and South America, with the latter region showing improved trends in the second quarter. The global businesses also delivered robust results, underscoring the value of the group’s extensive global and cross-border network. Notably, revenue growth was particularly remarkable in Santander CIB, witnessing a growth of 24%, as well as in Wealth Management & Insurance with a 25% increase, and in PagoNxt with an impressive growth of 27%. These figures demonstrate the bank’s effective strategic positioning and successful execution of its business initiatives across key sectors.

Santander Europe

During the first half of the year, the group achieved an attributable profit of €2,536 million, marking a substantial increase of 40%. This growth was primarily driven by strong profit performance in key markets such as Spain, the UK, Portugal, and Poland. In Spain, attributable profit surged by an impressive 74%, reaching €1,132 million, while in the UK, it saw a solid increase of 16%, reaching €818 million.

The bank remained focused on accelerating its business transformation in the region, implementing shared products and services, including a common mobile banking app. These initiatives contributed to higher growth in customer activity and income, while also leading to a more efficient operating model.

In terms of financial metrics, deposits experienced a 1% overall growth (with Spain contributing to a 3% increase). However, loans saw a decline of 5% (with Spain and the UK experiencing decreases of 6% and 4%, respectively) due to lower demand and early debt prepayments.

The bank’s strong emphasis on efficiency and cost management resulted in notable efficiency gains, particularly in Spain and the UK. Additionally, the bank was able to control costs below inflation. The cost of risk remained stable at 0.42%, reflecting the bank’s prudent approach to risk management during this period.

Overall, the bank’s performance in these key markets has been noteworthy, with significant profit growth, efficient operations, and a focus on enhancing customer experience through digital initiatives.

Santander North America

In North America, the attributable profit amounted to €1,346 million, showing a decrease of 19%. This decline was mainly due to the post-pandemic normalization in US auto provisions, as previously highlighted in the bank’s reports. Despite this, the region saw a strong performance in Mexico, where profit increased by an impressive 23%, reaching €760 million.

The second quarter brought positive developments for the bank in the US, as there was a decrease in provisions compared to the first quarter, signaling better-than-expected credit quality. This contributed to a 13% increase in profit for the region during the second quarter when compared to the first quarter.

Loans in the North American region experienced a 5% overall increase, with the US and Mexico contributing to growth rates of 6% and 3%, respectively. Deposits also showed strong growth, rising by 13% in the region, with both the US and Mexico contributing to growth rates of 13% and 11%, respectively.

The bank continued to strategically target segments with proven competitive advantages and actively promoted strong contributions from its group network in both Mexico and the US. At the same time, the bank focused on rationalizing businesses and products with limited scale and profitability to generate efficiencies and drive profitable growth in the region.

Overall, despite the decline in attributable profit for North America, the bank’s strategic focus on key segments and its efforts to optimize operations reflect a balanced approach aimed at enhancing profitability and long-term growth prospects in the region.

Santander South America

Attributable profit in the region declined by 23%, amounting to €1,458 million. This decrease was primarily driven by lower profits in Brazil and Chile. However, there were positive developments in other countries, namely Argentina, Uruguay, Peru, and Colombia, where the bank’s performance improved.

In Brazil, the attributable profit was €823 million, marking a significant decline of 40%. This decline can be attributed to several factors. While the region experienced strong customer growth and good performance in net fee income, these positive aspects were offset by an increase in costs driven by inflation. Additionally, there was a fall in net interest income due to negative rate sensitivity and a shift in the bank’s loan mix toward higher quality assets. Despite these challenges, the macro outlook in Brazil is showing signs of improvement as inflation slows down, and interest rates are expected to decrease in the near term this year.

The bank continued to focus on increasing connectivity across the region and made progress in its digital transformation efforts, aimed at enhancing efficiency and profitability. Despite the decline in profits, loans and deposits in the region saw an 8% overall increase, reflecting ongoing growth opportunities and customer confidence in the bank’s services.

In summary, while the region experienced challenges in some markets, there were positive trends in other countries. The bank remains committed to its digital transformation initiatives to drive efficiency, and with improving macroeconomic conditions, there are opportunities for further growth in the region.

Digital Consumer Bank

Digital Consumer Bank, which comprises Santander Consumer Finance (SCF) and Openbank, reported an attributable profit of €521 million, showing a decline of 7%. This decrease was mainly attributed to lower fee income and the impact of a temporary bank levy in Spain.

To counter these effects, the bank has shifted its focus towards new business pricing and profitability, as well as implementing measures to increase customer deposits and enhance operating efficiency. Despite the challenges, the cost of risk remained low at 0.54%, reflecting the bank’s prudent risk management practices.

Strategic alliances, leasing, and subscription services have played a significant role in driving new lending, leading to a 5% increase in this area. Among the largest markets contributing to profit were the Nordic countries with €137 million, the UK with €96 million, France with €94 million, and Germany with €84 million.

Overall, despite the decline in attributable profit for the Digital Consumer Bank, the bank’s proactive measures to optimize its operations and capitalize on growth opportunities reflect its commitment to adapt to changing market conditions and deliver value to its customers and shareholders.

Santander CIB

The Santander Corporate & Investment Banking (CIB) division witnessed remarkable growth, as attributable profit surged by an impressive 28%, reaching €1,876 million. This substantial increase was fueled by double-digit income growth across its core businesses, most notably in Global Transactional Banking, Global Debt Finance, and Markets. These successes allowed the unit to capture a larger market share. Santander CIB’s achievements were evident, as it ranked at the top of the league tables for European and Latin American corporate issuers in US dollars.

Wealth Management & Insurance, which encompasses the group’s private banking, asset management, and insurance businesses, also delivered a stellar performance. The division’s attributable profit experienced a substantial growth of 70%, amounting to €819 million. Private Banking was a standout performer within this segment, achieving outstanding growth driven by higher net interest income and strong commercial activity levels. Notably, Private Banking attracted a net new money inflow of €6.4 billion and increased its customer base by 10%.

Santander Asset Management, another component of Wealth Management & Insurance, demonstrated solid growth in net sales, reaching €3.2 billion. This success further contributed to the division’s overall strong financial performance.

Additionally, PagoNxt, the unit that encompasses Santander’s most innovative payments businesses, achieved a noteworthy increase in total income, growing by an impressive 27% to €521 million.

Overall, the exceptional performance of these divisions showcases Santander’s strong presence and success in various financial markets and highlights the bank’s commitment to providing innovative and efficient solutions to its customers.

Santander stock exchange price

Historic Santander stock price

If you are looking for a trading plattform check our top of brokers